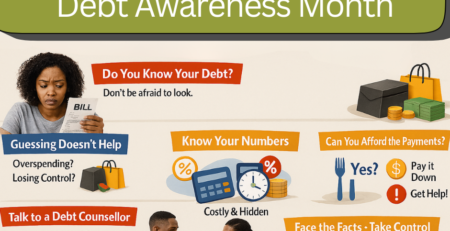

Is your Credit Life Insurance silently Draining your Wallet

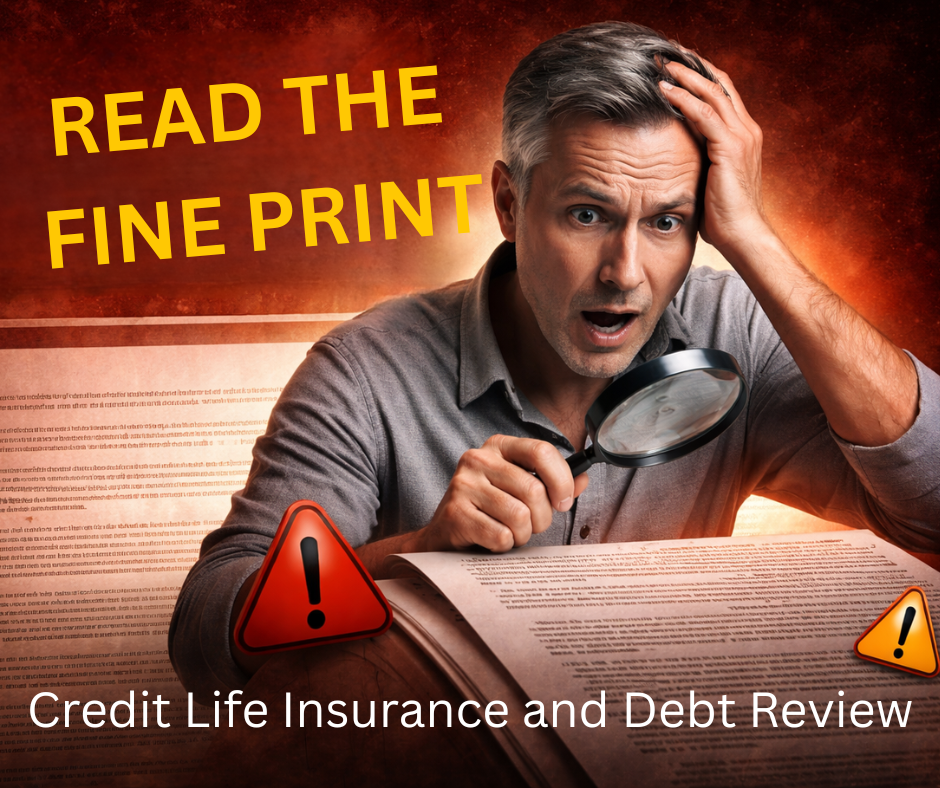

Why Reading the Fine Print on Credit Life Insurance (CLI) Is Critical.

Is your Credit Life Insurance silently Draining your Wallet

When entering debt review, one of the most overlooked yet financially dangerous components of any credit agreement is Credit Life Insurance (CLI) linked to your bond, vehicle finance, or personal loan.

Many consumers assume they are “covered.” The reality is: the fine print determines whether the insurer will actually pay when it matters — and how much you’re overpaying in the meantime.

1️⃣ What Is Credit Life Insurance?

Credit life insurance is a policy attached to a credit agreement that settles or services your debt if certain events occur, such as:

- Death

- Disability

- Retrenchment

- Temporary inability to work

Under the National Credit Act (NCA), a credit provider may require insurance but you have the legal right to choose your own insurer, provided the alternative policy offers like-for-like cover that meets the bank’s minimum requirements.

This is where many consumers lose money unnecessarily.

2️⃣ Why the Fine Print Matters — Especially During Debt Review

When under debt review, affordability is already tight. A rejected claim or an overpriced policy can destabilize your entire repayment plan.

⚠️ A. Retrenchment Cover Limitations

Many policies:

- Exclude voluntary retrenchment

- Exclude contract workers or directors

- Have waiting periods (6–12 months)

- Limit payout duration

⚠️ B. Disability Definitions

Some policies only pay for:

- Permanent total disability

- Inability to perform any occupation

Temporary disability may only pay for a few months.

⚠️ C. Pre-Existing Conditions

Failure to properly disclose, even years ago can lead to:

- Claim repudiation

- Delayed payout

- Partial settlement only

⚠️ D. Bond-Linked Insurance Risks

If your home loan is with a major bank such as:

- Standard Bank

- Absa

- Nedbank

- FNB

You must confirm:

- Does the policy settle the full outstanding balance?

- Or does it only cover instalments?

- Does the premium reduce as your balance reduces?

- Or does it increase annually regardless of your decreasing risk?

Many bank-linked policies increase premiums yearly even though your loan balance reduces. This is a critical fine print issue most consumers never question and as a result this even affects your overall repayment of the actual credit as yoru capital balance is affected.

3️⃣ The Overlooked Right: You Can Replace Expensive Bank Insurance

Under the National Credit Act, you are legally entitled to substitute the bank’s insurance with a like-for-like replacement policy, provided it meets the minimum required cover.

This is not optional goodwill from the bank it is your statutory right.

Specialist replacement providers such as:

- DC Credit Protect (DCCP)

- One Insurance

Offer compliant replacement policies that are often:

✔ Significantly cheaper ✔ Structured correctly for debt review ✔ Based on reducing balance cover ✔ Premium-adjusted downward as your balance decreases

Unlike many bank-linked policies:

- Premiums do not automatically escalate annually

- Premiums are not added annually to your capital balance so in effect the bank charges interest on insurance. (NOT ALL BANKS)

- Premium reduces in line with your outstanding debt

- You are not penalised for reducing risk

Over a 20 year bond or 6 year vehicle agreement, the savings can be substantial often tens or even hundreds of thousands of rand.

4️⃣ Why This Is Even More Important in Debt Review

During debt review:

- Every rand affects affordability.

- Overpriced insurance reduces your available repayment distribution.

- Inflated premiums slow down rehabilitation.

- A lapsed policy can collapse your restructuring.

Replacing high-cost insurance with a compliant alternative:

- Improves cash flow

- Reduces long-term cost

- Strengthens the sustainability of your repayment plan

5️⃣ What You Should Always Check in the Fine Print

✔ Waiting periods ✔ Retrenchment definitions ✔ Disability criteria ✔ Pre-existing condition clauses ✔ Premium escalation structure ✔ Whether cover is fixed or reducing ✔ Cancellation rights ✔ Your right to substitute with compliant cover

6️⃣ The Hard Truth

Many consumers only discover:

- They were overpaying for years

- Their retrenchment claim is excluded

- Their disability doesn’t qualify

- Or their premium increased annually without justification

Only at claim stage, when it is too late.

Debt review offers legal protection. But it does not override insurance exclusions or poor policy structuring.

Bottom Line

Credit life insurance should protect you, not silently drain your affordability.

Understanding your rights under the National Credit Act, Insurance Act, The Final Credit Life Insurance Regulations and exercising your option to replace expensive bank-linked insurance with compliant providers like DC Credit Protect or One Insurance can materially improve your financial recovery.

The fine print is not small……………………………………